What is a SAFE note? And why AI startups love them

SAFE notes have become the default instrument for early-stage AI fundraising. Here's what they are, the 2018 post-money switch, and what founders miss.

By Elena Kowalski, Insightful AI Desk

Almost every AI startup that has raised money in the last two years has, at some point, signed a SAFE. The instrument is so dominant at the early stage that many founders only encounter it for the first time when their lead investor sends over a draft, assuming it is a standard, assuming the terms are vanilla, assuming the round will simply close. Some of those assumptions are correct. Others are not, and the difference can be tens of millions of dollars on the cap table by Series B.

SAFE stands for “simple agreement for future equity.” It is a financing instrument introduced by Y Combinator in late 2013 and substantially revised in 2018. Y Combinator publishes the canonical form, gives it away for free, and offers three current US variants plus international versions for Canada, the Cayman Islands, and Singapore. This piece walks through what the instrument actually is, what the 2018 revision changed, and what an early-stage founder or angel should look for before signing.

What a SAFE actually is

A SAFE is not a loan, and it is not, by itself, equity. It is a contractual promise that the investor’s money will convert into shares of preferred stock at some defined future event, almost always the next priced equity round of a certain size, or a sale of the company. Until that event the SAFE sits on the cap table as a pending conversion. There is no interest accruing. There is no maturity date. There is no debt schedule. If the conversion event never happens, the investor’s money does not automatically come due; their recovery depends on what is in the agreement.

The original 2013 design was an explicit response to the convertible-note instruments that dominated early-stage fundraising at the time. Convertible notes are technically debt: they have an interest rate, a maturity date, and a legal obligation to repay if not converted. For early-stage companies whose finances are aspirational, all three of those features create problems. The SAFE strips them out. What is left is a much smaller piece of paper that mostly describes the conversion math.

The simplicity has trade-offs. Without a maturity date, an early investor has weaker leverage if the company never raises a priced round. Without interest accrual, the investor’s effective return depends entirely on the conversion price they negotiate up front. The exchange of those protections for legal and operational simplicity is the deal the SAFE makes.

The 2018 revision: pre-money versus post-money

The most consequential change Y Combinator made to the SAFE was the 2018 switch from pre-money to post-money as the default valuation framework. The distinction sounds technical and is, to anyone signing one without reading carefully, the single most important thing in the document.

A pre-money SAFE sets the valuation cap or discount as a pre-money figure. When the SAFE converts at the next priced round, the dilution from the SAFE’s own conversion (and from other SAFEs converting alongside it) is shared with the round’s new investors. Early SAFE holders effectively benefit from a moving denominator.

A post-money SAFE, the current YC default since 2018, sets the cap or discount as a post-money figure that already includes the converting SAFEs themselves. The SAFE holder’s percentage of the company is fixed at the moment of conversion in a way the pre-money version was not. The new priced-round investors bear all of the dilution that comes from converting the SAFEs.

YC’s framing for the change is on its current documents page: the post-money structure reflects the reality that early-stage seed rounds had grown large enough to behave like priced financings on their own, rather than bridges to a later Series A. The instrument was rewritten to match the world it was being used in.

For founders the practical implication is large. A founder who stacks several post-money SAFEs at different caps before raising a priced round can end up significantly more diluted at the priced round than the same founder doing the same nominal amount of fundraising on pre-money SAFEs. The instrument’s default mechanics now favour the SAFE investor more than the older default did. This is the policy YC chose, in the open, when it changed the form. It is also one of the most common gaps in founder understanding of an instrument they assume is standard.

The three US variants

Y Combinator’s current public form offers three variants of the post-money SAFE in the United States. The choice between them determines how the conversion price is calculated.

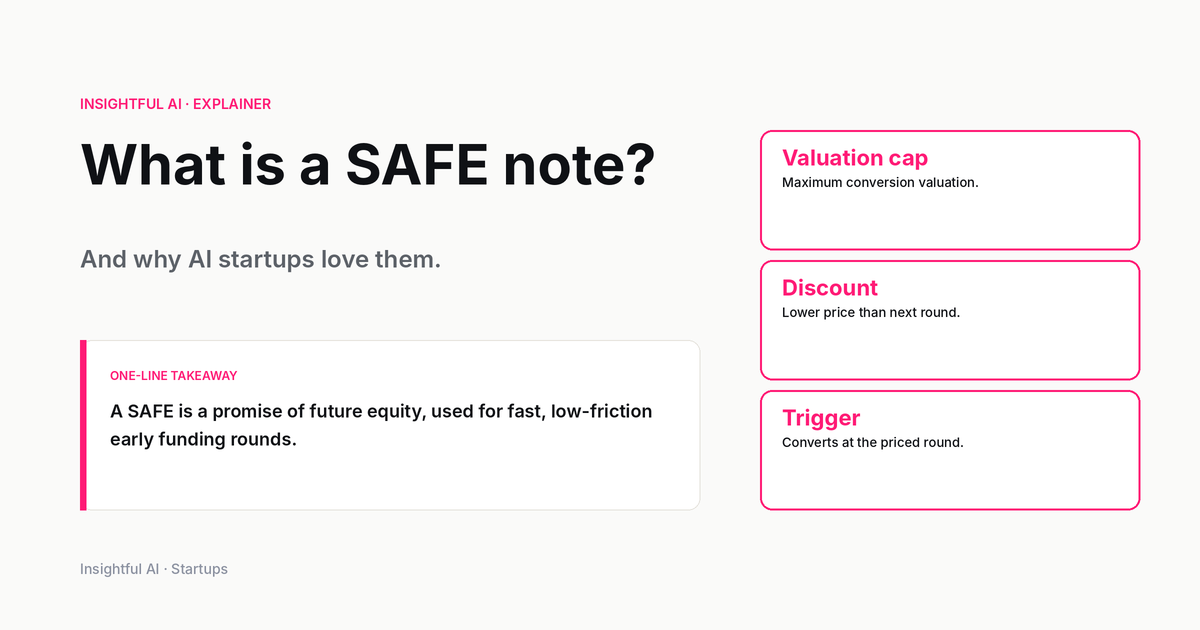

- Valuation Cap (no Discount). The SAFE converts at the lower of the next round’s priced valuation or the cap stated in the SAFE. The cap is the maximum effective valuation the SAFE investor will pay; if the next round prices above the cap, the SAFE investor gets a bargain.

- Discount (no Valuation Cap). The SAFE converts at a percentage discount to the next round’s priced valuation. The investor pays less per share than the new-round investors, but does not benefit if the company’s valuation runs away.

- MFN Only. The SAFE has no cap and no discount of its own. Instead, if the company subsequently issues another SAFE with more favourable terms, the MFN holder gets to convert under those terms automatically. The MFN variant is essentially a delegation of price-discovery to whichever investor negotiates the hardest later.

In practice the Cap variant dominates. Discount-only and MFN-only SAFEs exist but are less common, particularly in well-known accelerator programmes where investors expect both a cap and the possibility of MFN protection negotiated as a side letter.

Why startups (and AI startups especially) use them

Three operational reasons explain why SAFEs displaced convertible notes for most early-stage rounds.

The first is legal cost and speed. A SAFE is a few pages of standard form. There is no debt covenant negotiation, no interest-rate haggling, no maturity-date back-and-forth. A founder can close a SAFE in a week with minimal legal work. For a company that is mostly burning cash to hire engineers and rent GPU time, the saved legal fees are not trivial.

The second is cap-table delay. Because the SAFE does not convert into actual shares until the priced round, the company does not have to admit new equity holders to the cap table until then. There is no immediate need to issue stock certificates, no board notices, no transfer paperwork. The administrative load arrives only when the priced round closes.

The third reason is specific to the current moment: AI valuations are volatile. Founders raising at the white-hot end of the AI market often prefer to defer pricing the round until the market has had more time to clarify. A SAFE with a high cap (or no cap, in the MFN variant) lets the company take money now and let the priced round set the actual valuation later. This is the same logic that made convertible notes popular in earlier cycles, with one less moving part.

What founders give up

The SAFE’s simplicity comes at costs that show up later.

The first is stacking dilution. Multiple SAFEs at different caps, especially post-money SAFEs, can stack their dilution in non-obvious ways. A founder who has signed three SAFEs at three different caps will not, intuitively, know their pre-round ownership without doing the math. A surprising number of founders only discover their actual dilution when the Series A closing-table model is built. The fix is to maintain a running SAFE-conversion model from the day the first SAFE is signed.

The second is investor protections that escalate at the priced round. Post-money SAFEs convert into preferred stock with the protections preferred stock typically carries: liquidation preferences, anti-dilution, sometimes pro-rata rights. Founders who think they have signed a simple paper often discover at the priced round that the SAFE has now become the company’s most senior class of equity.

The third is information rights, side letters, and the cap-table complication. A SAFE does not automatically include investor information rights or board observer seats, but those are often negotiated as side letters. Several SAFEs from several investors can produce several side letters with mismatched terms. Cleaning this up at the Series A is its own legal sub-project.

What investors give up

For balance, the costs on the investor side are real too.

The absence of a maturity date means the investor’s money has no defined return event other than the next priced round or a sale. A company that never raises another round and never sells leaves the SAFE investor with a position that is hard to value and harder to exit.

The absence of interest means the time value of the investor’s capital is borne entirely through whatever discount or cap they negotiated. If the company takes three years to reach a priced round, the SAFE investor has effectively given an interest-free loan.

The absence of debt covenants means the investor has limited contractual control over how the company spends the money. Most early-stage investors are not seeking that control, but it is worth knowing the structure they are signing.

What to ask before signing

For a founder receiving a SAFE term sheet, four questions move most of the actual money on the table.

Is the SAFE pre-money or post-money? The 2018 YC default is post-money; non-YC instruments may still be pre-money. The dilution math differs materially.

What is the valuation cap, and what comparable rounds is it benchmarked against? A cap without a comparable is a number floating in space.

For an angel or seed investor on the other side of the table, two more questions.

What other SAFEs are outstanding, and at what caps? Stacked SAFEs can change the effective dilution of the round being negotiated.

What is the company’s realistic timeline to a priced round? Because the SAFE has no maturity, this timeline is the only meaningful constraint on when the investor’s position converts.

None of these questions require legal training to ask. They are the questions that, if not asked up front, become the awkward conversations at the Series A closing table.

Further reading: the canonical reference is Y Combinator’s documents page, which publishes the current SAFE forms in all three US variants plus international versions, all free to download. For a deeper read on the 2018 post-money revision and its dilution consequences, the YC blog post announcing the change covers both the mechanics and YC’s rationale.

How we use AI and review our work: About Insightful AI Desk.